Republished

from Scoop Media

Chris Sanders: Where is the Collateral?

Tuesday, 28 October 2003, 10:11 am

Column: Chris Sanders

Where is the Collateral?

By Chris Sanders

Sanders Research Associates

"The more restrictions and prohibitions there are, the poorer the

people become

The sharper the people's weapons are, the more national confusion

increases

The more skill artisans require, the more bizarre their products

are

The more precisely laws are articulated, the more thieves and outlaws

increase"

- Lao Tzu, Tao Te

Ching

"F**k you!"

- Michael Eisenson,

Harvard Endowment, to Hamilton Securities CEO

Catherine Austin Fitts

Catherine Austin Fitts

Real terrorism

On the 29th of October, a trial begins in a Federal courtroom in Washington DC. The defendant in the case is our own distinguished advisory board member Catherine Austin Fitts. The plaintiff in the case is one John Ervin of Ervin Associates, a mortgage servicer for HUD. Ervin has brought the case using a Federal whistle blower statute (qui tam) [i] that allows private citizens to bring suit against parties alleged to have defrauded the government, and rewards them with a percentage of the recovered money. Ervin began eight years ago with more than 30 offences alleged against Fitts. He is now down to a handful, technical and immaterial in their financial impact one way or another on the government, Fitts, or anyone else. The case is ironic in many respects. Fitts, a HUD contractor, was fired "for convenience," which does not mean that she was terminated for wrongdoing. Ervin and Associates themselves were fired some time back by HUD "for cause," meaning that they were fired for non-performance under a contract. Yet here Ervin is taking Fitts to court, ostensibly on behalf of the government and taxpayer.

This is the first time in eight years that Fitts has had an opportunity to defend herself in a court of law after millions of dollars in legal expenses, her company bankrupted by the failure of HUD to pay it for completed and accepted work and her personal savings destroyed. In the process, far from establishing that she or her company committed any wrongdoing, it has been established that HUD itself falsified evidence. In the words of one Senate staffer knowledgeable about the Department of Housing and Urban Development, "HUD is being run as a criminal enterprise." [ii]

Investors should pay very close attention to the conduct and outcome of this trial, because the issues involved have far wider market and economic ramifications than whether or not Fitts is convicted of something. The mere fact that it has taken eight years to get into a courtroom is reason enough to wonder about both the merits and conduct of the case. The fact that the HUD Inspector General dropped its investigation of Fitts and Hamilton in 2001 after admitting that it could find no evidence of wrongdoing is another. [iii] The fact that the Department of Justice declined to take up Ervin's qui tam in 2000 suggests real doubts as to the merits of the case. The fact that Federal Judge Stanley Sporkin systematically violated the whistleblower statute itself for six years by repeatedly granting extensions to the legally limited 60 day seal on the plaintiff's "case" against Fitts is another telling sign of the real truth: there is no case against Fitts. Can you imagine being accused, but never able to know what you have been accused of? And the haste with which the Department of Justice seized the records and erased the hard discs of the computers of Fitts' firm, Hamilton Securities, meant that for all intents and purposes the firm was destroyed with no recourse. How do you pursue recourse when you don't know what you are pursuing recourse against? Now the fact that Sporkin used to be chief counsel for the CIA is really neither here nor there. Or is it? [iv]

The truth behind privatisation and transparency

The question is relevant because the business that Hamilton was engaged

in was managing the sales of defaulted loans for HUD. The historical recovery

rate on the defaulted loan portfolio was about a third. Fitts and Hamilton

nearly tripled that by gathering and publishing place-based data for the

localities in which the underlying collateral was located. If you are

astonished that until Hamilton came along and did it, HUD was not able

(or was it unwilling?) to provide such data to potential investors, you

are not alone. But the astonishing fact is that HUD never operated a system

that would allow the aggregation of data in such a way as to match operations,

expenditures, revenues and locations. By gathering, processing and aggregating

place-based data, Hamilton made great strides (as an outside contractor

no less) towards doing this. And at the same time, Hamilton opened up

the bidding on the defaulted loan portfolio to a wider group of potential

buyers.

The question is relevant because the business that Hamilton was engaged

in was managing the sales of defaulted loans for HUD. The historical recovery

rate on the defaulted loan portfolio was about a third. Fitts and Hamilton

nearly tripled that by gathering and publishing place-based data for the

localities in which the underlying collateral was located. If you are

astonished that until Hamilton came along and did it, HUD was not able

(or was it unwilling?) to provide such data to potential investors, you

are not alone. But the astonishing fact is that HUD never operated a system

that would allow the aggregation of data in such a way as to match operations,

expenditures, revenues and locations. By gathering, processing and aggregating

place-based data, Hamilton made great strides (as an outside contractor

no less) towards doing this. And at the same time, Hamilton opened up

the bidding on the defaulted loan portfolio to a wider group of potential

buyers.

Imagine that. Hamilton made the process of default resolution more transparent and less cosy and raised the cost of buying defaulted loans considerably. No wonder that Fitts angered certain people and institutions. If you stop and reflect on what Hamilton's actions meant from the standpoint of cash flow and profit, you will see what I mean. The impact was to raise the amount recovered by HUD (i.e. the taxpayer) by over $2 billion, which means in effect, to reduce the profit that would have gone to the likes of the Blackstone Group, Goldman Sachs, GE and Harvard by at least that much. Stick a multiple of say, eighteen on the stock price of the exchange traded firms and you begin to see what sort of impact that would have. And one can surmise from the reaction of Harvard's Eisenson quoted above what the impact on Harvard's investment in its HUD servicing companies NHP and WMF would be. [v]

One might well ask what Robert Rubin as Treasury Secretary saw in AMS Technology and its founder and chief executive officer Charles Rossotti who were brought into HUD (at about the time that Hamilton was being taken down) to replace HUD's computer software and systems. Against all auditing standards they replaced them with no parallel runs. The unsurprising result was that within two years HUD had nearly $60 billion in "undocumentable transactions." Undocumentable transactions?! Where is the money? HUD cannot (or will not) tell you, and indeed, it cannot tell its GAO auditors either, which is why it did not and does not pass audits, in much the same style of Bill Cohen's and Donald Rumsfeld's Defense Department, which amassed over $2.5 trillion in "undocumentable transactions" before they stopped telling people what the amount is. [vi]

The upshot of this is the spectacle of HUD firing a contractor (Hamilton and Fitts) that saved them over $2 billion, and rewarding a contractor (AMS and Rossotti) that has lost them at least $60 billion. Indeed, Rossotti's work was apparently held in such high regard that he was made Commissioner of the Internal Revenue Service in Rubin's Treasury, from which vantage point he managed to secure a Treasury contract for AMS. [vii]

Inflating the credit bubble...

HUD did not just fire Hamilton, it also abolished the defaulted loan sales program in 1997 that Hamilton had so successfully created and run for it. The result was predictable, as the recovery rate on defaulted loans fell back to where it had been before Hamilton's loan sales program. This did not stop HUD from continuing to use the higher recovery rate under the old loan sales program run by Hamilton as the basis for calculating the loan loss reserves for new loan origination and insurance volume. This allowed HUD to greatly expand the volume of its loan and insurance business. So great was this expansion, in fact, that even at the time some observers worried that there was not a big enough market to absorb the new loans.

Now if, for the sake of example we assume that the recovery rate under Hamilton was 75% on every $100 million, and that volumes were doubled thereafter while the recovery rate fell to 30%, then the losses to the taxpayer would rise from $25 million to $140 million. Sadly, this is the sort of loss rate that HUD must in fact be experiencing on a portfolio worth billions. You may well ask yourself how something like this could be allowed to happen, that surely someone in government would blow the whistle.

This is a reasonable question, and it has an equally reasonable answer. The fact is that they don't blow the whistle because they either do not know or do not want to. Susan Gaffney, HUD Inspector General, when questioned about the loan sales recovery and loss rates, flatly stated that she did not know and did not see why she should know. The IG, mind you, is the internal audit and control officer of HUD. This is reminiscent of a similar complicity at the Pentagon's IG office, which in the spring and summer of 2001 was under congressional investigation for the fraudulent issuance of credit cards to phantom employees. This investigation died in the explosions on the 11th of September that year, as did so many people.

But the cupidity of the HUD IG alone is not enough to explain the default of oversight and its continuing cover up. The reorganisation of HUD's regional offices does, however, go a long way to filling this gap in our understanding. These offices were consolidated into two centres nation wide, resulting in the redundancy, dismissal and transfer of staff, effectively destroying the institutional memory of the organisation and consolidating ongoing operations into a few trusted and more easily controlled hands.

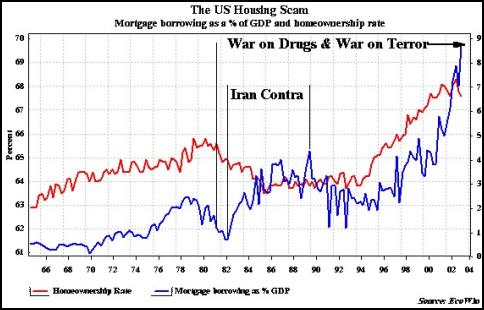

Establishing exactly what is going on at the Federal Housing Administration is very hard to do from the outside. What we can see more easily is the meteoric expansion in mortgage debt outstanding in the United States, which has far outpaced GDP growth in the years since Hamilton Securities was fired by HUD. At the beginning of 1996, the annual rate of increase in mortgage borrowing in the United States was about $200 billion. That has increased to $900 billion by mid 2003, representing an increase from near 2.5% of GDP to about 8.75% of GDP in the same seven year period, or a more than four-fold increase. The home ownership rate has increased by 2.5% in the same time. What is going on?

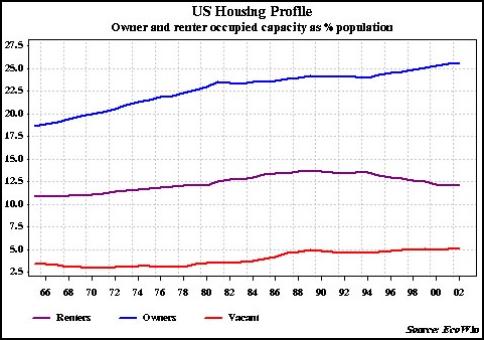

The total proportion of owners and renters has not changed materially in more than ten years, which leads to the inference that the rise in the homeownership rate has been due solely to renters buying homes. This is unsurprising given the drop in interest rates to levels not seen in more than a generation. This may account too for at least some of the rise in housing vacancy rates if previously rented accommodation is empty because of a dearth of demand. But this cannot begin to explain the huge rise in the annual rate of increase in mortgage volume. Nor does refinancing explain it; for every loan refinanced another drops out.

The government sponsored enterprises that form the core of the industry of American home finance have been under attack for several years now. Not only have they enjoyed market pricing for their debt that is based on the assumption that the government stands behind it, but they have also benefited from direct lines of credit from the Treasury. Fannie Mae and Freddie Mac have consequently had a competitive advantage unmatched (and indeed, unmatchable) in the private sector. It is no exaggeration to say that the taxpayer has made possible the meteoric expansion of Fannie and Freddie's balance sheets.

...and hiding the pump.

It is curious therefore that as we reported in November and December 2001, Congress passed legislation allowing Ginnie Mae, the lending arm of the Federal Housing Administration at HUD, to compete for the first time in the commercial market for loans and guarantees with Fannie and Freddie. We are moved to wonder anew about this legislative action in the light of the criminal investigation of Freddie Mac's management launched this summer. Was this anticipated in the autumn of 2001 and was the opening of the commercial market to Ginnie Mae intended to make possible the continued expansion of the national mortgage portfolio behind the shield of the FHA and its refusal to disclose essential financial information? To be blunt, is this just a wheeze to hide fraud?

Fannie and Freddie have worked for years now in a curious legal environment which has allowed them not just a competitive advantage but has also allowed them to translate this into a stock market multiple that has been the envy of their commercial and mortgage banking competitors. The fact alone that they are able to access the stock market increases the amount of disclosure that they must make. But the advent of the new Basel Accord on banking supervision and capital adequacy makes is doubly difficult. Foreign central and commercial bankers have been unhappy for some time with the financing advantages accorded to the GSEs, which were rated as risk free equivalents to Treasury bonds under the original Basel I Accord. This has meant that banks holding GSE paper have not had to hold any capital against it, creating a large incentive to buy GSE paper instead of treasuries or other government debt.

As desirable as it is to clip the wings of the GSEs and to force them to compete on the same basis as their commercial rivals, there is real reason to be concerned about the expansion of Ginnie Mae's brief at the FHA in light of the inability of the FHA and HUD to operate on anything like a transparent basis or to perform even the most basic of fiduciary obligations.

What is going on? This is a question that every central banker in the world should be asking as he contemplates the level of exposure of his national reserves and his domestic banking system to US agency risk. Is there really matching collateral behind the huge increase in outstanding mortgage debt in America today? It was Hamiltion Securities that provided the sort of place-based information that would have answered this question. We can't prove that the collateral isn't there, at least yet. But what is really scary is that HUD cannot prove that it is.

Think about it.

- Chris Sanders

See the sequel to this article:

So, Where is

the Collateral?, July 2004

FOOTNOTES:

[i] "Qui tam" lawsuits are authorised under the Federal False Claims Acts and are brought by citizens (called "relators" or "whistleblowers") who allege wrongdoing and misuse of government funds. They are allowed to keep a percentage of any monies collected. Revenue from such activities has become an increasingly significant part of the government's finances, as have related activities involving asset forfeiture revenues. Understanding this is fundamental to understanding the motivation behind the Hamilton case. It is significant in our view that Dyncorp (now part of Computer Sciences Corporation - CSC, NYSE), which is a prime contractor for the Justice Department running its asset forfeiture program, is a also a contractor for HUD running computer systems. In 1996, Dyncorp was paid $60 million and generated $450 million in asset forfeiture revenues. Hamilton was paid $10 million and generated $2.2 billion in savings for HUD.

It is difficult to avoid the conclusion that the cash generating activities associated with enforcement are more desirable to the managers of the system because they are easier to manipulate than running the system for a positive return to the taxpayer.

[ii] Chief of Staff to Senator Kit Bond (then chairman of the Senate subcommittee on HUD appropriations) to Fitts in 2000.

[iii] This was shortly after the publication of an article on the case by Paul Rodriguez of Insight Magazine and resulted as well in the resignation of HUD IG Susan Gaffney.

[iv] A recurring theme in the Hamilton story is the prominence of a small number of contractors in IT and financial control across the federal government, including Lockheed Martin, Dyncorp and AMS, covering the DOD, DOJ, HUD, the SEC, State Department and Treasury. On the face of it this may not seem like a big deal. However the failure of the two biggest agencies -- HUD and DOD -- to pass audits raises material questions about the contractors, their role, and their performance.

[v]It is noteworthy that Pug Winokur, member of the board of Harvard Endowment was also on the boards of NHP and WHF, as well as being on the board of Dyncorp, a HUD contractor. Winokur was replaced last year Harvard's board by former Treasury Secretary Robert Rubin.

[vi]This is presumably because to divulge such information to the American public that pays them is considered a national security risk in the age of "terror," and is a clue to those who are puzzled by war on terror as to what its real objectives are.

[vii]Rossotti was also granted an exemption

in order to permit him to retain his large personal position in AMS stock.

If you will recall the furore over the personal stock holdings of members

of the incoming Bush Administration, you may well wonder at the ironies

of public life.

Copyright (c) Scoop Media

See also the sequel to this article:

So, Where is

the Collateral?, July 2004

|

|